*Rod Griffin, Director of Public Education for Experian

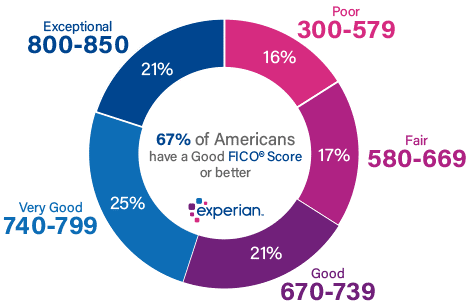

FICO scores are used in 90% of lending decisions, so those ranges are listed below, using estimates from Experian.

- Very poor:300 to 579

- Fair: 580 to 669

- Good:670 to 739

- Very good:740 to 799

- Excellent: 800 to 850

Credit Crisis

A good credit score can help you receive better-than-average APR’s (Annual Percentage Rate) (the interest you pay) from lenders and increased approval odds for credit. With good credit, you have better chances at qualifying for a mortgage, lease or car loan.

“Making payments on time and keeping your balances low are the two most important factors when it comes to building credit,” Griffin says. Building credit takes time.

In fact, payment history is the most important factor making up your credit score. A whooping 35% over-all. Your credit score considers whether you make payments on time or late and if you carry a balance month to month or pay it off in full.

Even if your credit score falls within the good range, that is not a guarantee you’ll be approved. Lenders and Credit Card issuers look at more factors than just your credit score, including but not limited to, your income and monthly housing payments.

Borrowing beyond your means is perhaps the fastest way to make your credit score plummet. The lower the credit score the more in Interest you will pay, if you qualify at all. Your amount of outstanding debt may not have a direct impact on your credit score, but your ability to pay it off does.

Next time, How Credit & Debt Affect your whole financial life. Is there any way out of the Credit & Debt Crisis affecting your life?